WATCH & LEARN: Music has a unique way of capturing our hopes, dreams, and aspirations. But beyond songs, what are we doing today to make those dreams come true?

How to Protect a Business and its owner

November 19, 2017

A business succeeds or fails based on the owner’s commitment and ability to execute and manage his business plans well.

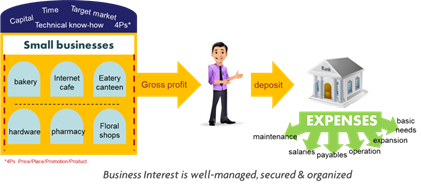

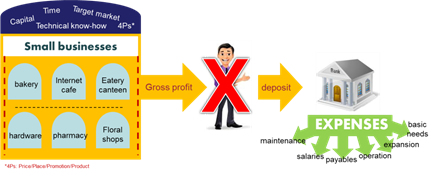

The Philippines is a highly entrepreneurial country. The main reason why most of us venture into small businesses is because majority of its citizens live below the poverty line. Starting a small business is one way to start one’s journey to accumulate and build wealth. There are a lot of small businesses opportunities that one can take, like an eatery, internet cafe, bakery, floral shops, to name a few. But choosing one that will surely be profitable and successful is a whole different story.

Usually, it takes time or years to establish a particular business. You need several components to make that happen:

- Capital: To practically finance and jump-start the business. This could be in a form of borrowings or loan.

- Time: Ideally, you need to dedicate yourself to fully-supervise your business operation

- Technical “know-how” : How well do you know your product line? If it’s a restaurant, how much do you know your chosen cuisine?

- Target Market: To whom do you cater your product? Profiling is also important to identify your potential customers

Remember, aside from the components mentioned above, you should have a real personal interest and passion in the business you will engage in. A business succeeds or fails based on the owner’s commitment and ability to execute and manage his business plans well.

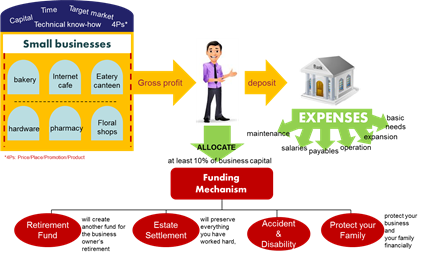

This is how a normal business cash flow works: See figure: 1