Please select a topic to ask questions about

- Beneficiary-related questions

- Claims-related questions

- Client information update

- Digital insurance (D.E.A.L) questions

- Electronic policy contract (ePolicy)

- General questions

- Insurance-related questions

- Investment-related questions

- Orphaned clients

- Paperless subscription

- Payment

- Policy service questions

- SIM card registration

- VUL-related questions

- VUL withdrawal questions

To change your beneficiary/ies, you’ll need:

- A duly-signed Change of Beneficiary form

- A copy of your valid ID

You can submit these requirements via any of the following channels:

My Sun Life PH Client Portal or Mobile App

- Log in

- Click Requests Manage beneficiaries

- Go over the reminders, then click Agree and proceed

- Select the policy whose beneficiary/ies you wish to change, then follow the steps on the succeeding screens

Your Sun Life Advisor

You can ask them to help you fill out the Change of Beneficiary form and submit your requirements on your behalf.

A Sun Life Client Service Center

You can find the nearest one on the Where to find us page.

To file a death claim, you require:

- Claimant's Statement

- Certified true copy of the Death Certificate (blue form is not acceptable) signed by the Local Civil Registrar with official seal, Local Civil Registry number and documentary stamps

- Other forms or documents which may be required at the time of claim.

You can inspect our checklist of requirements. Claimants will also receive a copy of the checklist as soon as the Company is notified of the claim.

To file a living benefit of a life insurance claim, you will need:

- Claimant's Statement

- Attending Physician's Statement

- Police Report (if applicable)

- Other forms or documents which may be required at the time of claim

Read how to file a claim for more details.

There are no requirements needed to claim your policy maturity benefit except when the claim will be made, on your behalf by your spouse or designated beneficiary who is a minor. Guardianship requirements under Philippine law should be submitted for a minor designated as the endowment/maturity beneficiary. If your spouse is the named endowment/maturity beneficiary, an NSO-issued marriage certificate is required.

A maturity notice will be mailed to the endowment/maturity beneficiary prior to maturity date.

The following documents are required for a living benefits claim:

- Claimant's Statement

- Attending Physician's Statement

- All documents related to the life insured's medical treatment

- Police Report (if applicable)

- Other forms or documents which may be required at the time of claim

Claims Related Questions

When you are filing a claim:

- Ensure that all your records are organized, updated and accessible. Additional documents may be required depending on the designation of beneficiary/ies in the policy contract.

- Check if your beneficiary designations are updated or consistent with your wishes especially in the case of a change in your status (e.g. from single to married).

- Immediately file a Release of Assignment as Collateral Security as soon as your mortgage/loan is fully paid to update your beneficiary designation.

- Submit all necessary documents as specified in the Claim Requirements Checklist

To file a death claim, you require:

- Claimant's Statement

- Certified true copy of the Death Certificate (blue form is not acceptable) signed by the Local Civil Registrar with official seal, Local Civil Registry number and documentary stamps

- Other forms or documents which may be required at the time of claim.

You can inspect our checklist of requirements. Claimants will also receive a copy of the checklist as soon as the Company is notified of the claim.

To file a living benefit of a life insurance claim, you will need:

- Claimant's Statement

- Attending Physician's Statement

- Police Report (if applicable)

- Other forms or documents which may be required at the time of claim

Read how to file a claim for more details.

There are no requirements needed to claim your policy maturity benefit except when the claim will be made, on your behalf by your spouse or designated beneficiary who is a minor. Guardianship requirements under Philippine law should be submitted for a minor designated as the endowment/maturity beneficiary. If your spouse is the named endowment/maturity beneficiary, an NSO-issued marriage certificate is required.

A maturity notice will be mailed to the endowment/maturity beneficiary prior to maturity date.

The following documents are required for a living benefits claim:

- Claimant's Statement

- Attending Physician's Statement

- All documents related to the life insured's medical treatment

- Police Report (if applicable)

- Other forms or documents which may be required at the time of claim

You can file a claim at these locations:

- Client Service Centers

- Sun Life Financial Advisor

- Client Care: (632) 8849-9888

- E-mail: #PHIL_Claims@sunlife.com

- Text/SMS to 0908-8968278

The Text/SMS should have the following format:

"SUNLIFE<space>CLAIMS<space>Insured's name/Date of birth/Type of claim"

Date of birth format: mmddyyy

Type of claim: Death or Others

e.g. "SUNLIFE CLAIMS Juan dela Cruz/09081965/Death"

View our updated list of Sun Life Financial Offices in the Philippines.

Read how to file a claim for more details.

Death claims meeting our “speedy“ case criteria are generally processed within twenty-four (24) hours from receipt of complete claim requirements.

Death claim processing for “non-speedy“ cases, however, takes longer to ensure sound and fair settlement.

Kindly get in touch with us through PHIL_Claims@sunlife.com for more details.

Read how to file a claim for more details.

For living benefits in a life Insurance claim:

- Life Insured/Owner

For Death Benefits:

- Death Beneficiary/ies

For Endowment/Maturity benefits:

- Endowment/Maturity Beneficiary/ies

Note: If no endowment/maturity beneficiary is designated, the Policy Owner will automatically receive the endowment/maturity benefit.

Claims are generally paid in the form of crossed checks. This protects your beneficiary since a crossed check can only be deposited to the account of the payee. Sun Life may also deposit claim proceeds directly to the bank account of the beneficiary upon receipt of appropriate Request form.

The client has several options to receive his/her claim:

- Pick up at a client designated Client Service Center.

- Send check through Advisor.

- Deposit to maturity beneficiary’s bank account upon receipt of signed Request Form.

Client Information Update

Need to update your personal info? Here’s everything you need to know.

You can update the following:

- Name

- Contact details

- Marital status

- Email ID

The steps vary depending on the details you wish to amend.

To update your name, you’ll need:

- Duly-signed Name Change Request form

- An original or certified true copy of a legal document* containing your correct or new name

- A copy of your valid ID

*Examples include birth certificates, marriage contracts, and adoption papers.

You can submit these requirements via any of the following channels:

My Sun Life PH Client Portal or Mobile App

- Log in to your My Sun Life PH Client Portal or Mobile App

- Go to Requests, then click on Change name.

- Choose the name that you want to update.

- Update the details, then choose on the Reason for change.

- Choose the document to be uploaded and upload the file.

- Check the summary of changes then tick on the Terms and Conditions.

- Click Submit.

Your Sun Life Advisor

You can ask them to help you fill out the Name Change Request form and submit your requirements on your behalf.

A Sun Life Client Service Center

You can find the nearest one on the Where to find us page.

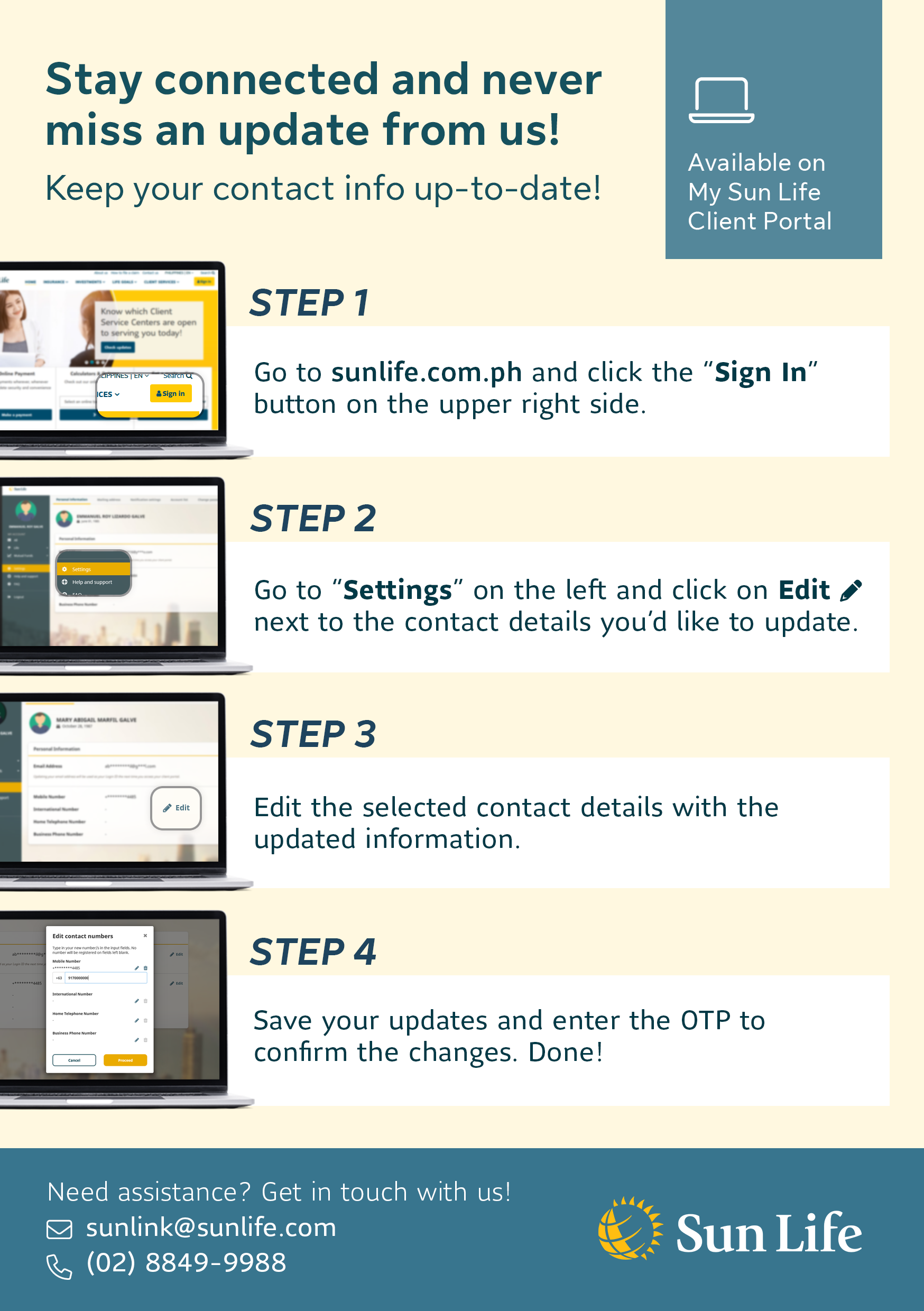

There are two ways to update your contact details:

Via the Client Portal or Mobile App

- Log in and go to Settings

- Click Contact info

- Click the edit icon next to the item you want to update, then follow the steps on the succeeding screens

Via your Sun Life Advisor or a Sun Life Client Service Center

Simply prepare and submit the following requirements:

- The back portion of your premium notice

- Signed letter of request

- Accomplished Address and Contact Information Change Request form

To update your email ID, just follow these simple steps:

- Log in and go to Settings

- Click Contact info

- Under Primary contact details, click the edit icon beside Primary email address, then follow the steps on the succeeding screens

Digital Insurance (D.E.A.L.) Related Questions

Digital. Easy. Affordable. Life Insurance (D.E.A.L) is Sun Life’s suite of digital insurance products. We envision touching more Filipino lives by making insurance as easy as possible.

Sun Life is developing digital distribution capabilities by collaborating with different industry players in financial technology and InsurTech that have good market base, solid value proposition, and high growth potential.

The following products comprise Sun Life’s D.E.A.L. suite:

- Byahero Protect – Group Personal Accident insurance that provides benefits for accidental death and accidental dismemberment; it also pays additional benefits for hospitalization and death due to accidents while travelling on land within the Philippines.

- Life Armor – Group One-year Term insurance that pays the full insurance coverage for deaths due to accidents or illnesses.

- Family Armor – Group Personal Accident insurance that provides accident coverage and reimbursement (subject to a set limit) of medical expenses for bodily injury due to an accident for the principal insured and his nominated dependents/family members.

- Personal Accident Armor – Group Personal Accident insurance that provides benefits for accidental death and accidental dismemberment.

*Terms and conditions apply. Should there be any discrepancy contained in this material and the insurance policy contract, the terms and conditions of the Group Insurance Policy Contract will prevail.

Availability is never an issue as these products are available through popular and trusted online platforms. Our digital insurance products (D.E.A.L.) are available in the following digital platforms:

- Lazada - the leading e-Commerce site in the country;

- Moneygment - a niche e-wallet player that caters to self-employed individuals, homemakers and the general unbanked population for the payment of their income taxes and government contributions like SSS, PhilHealth and Pag-IBIG;

- GCash - Leading digital wallet and financial lifestyle platform in the Philippines.

We continue to establish partnerships with widely used digital players that offer relevant and complementary services to make our digital insurance products accessible to more Filipinos.

Registered members of the digital partners (Lazada, Moneygment, and Gcash) who satisfy the eligibility requirements may avail of these products. For more information, please visit the platforms of Sun Life’s digital partners or call Sun Life Client Care at +632 8 849 9888.

Our digital insurance products are simple and easy to understand. Application is easy through a short online form. Activation instructions will be sent to your registered email after you have completed your purchase transaction from any of our digital partners.

Insurance coverage will start upon receipt of the electronic Proof of Cover (e-PoC), which is sent through the insured member’s nominated email address. The insured member must ensure that the email address supplied upon registration is valid and accessible. He/she may contact Sun Life Client Care: +632 8 849 9888 in case the e-PoC is not received within five (5) to seven (7) days.

Yes, insurance coverage may be cancelled within a period of fifteen (15) days from receipt of the e-POC. Once the insurance is cancelled, the premium will be refunded (less any online transaction fees charged by the digital partner). The insured member will be notified of the refund. In the event that the premium was charged to and paid for by the insured member instead of the group policyholder, the insured member will be entitled to a refund in accordance with the Group Insurance Policy Contract.

Insured members can get more information about Sun Life Philippines' suite of digital group insurance products by contacting Client Care through the following channels:

- Telephone: +632 8 849 9888; if calling from the province, the PLDT toll-free number is 1-800-10-SUNLIFE (1-800-10-7865433).

- Email: sunlink@sunlife.com

- Business Hours: Weekdays except holidays, 8:00 AM to 5:00 PM

Electronic Policy Contract (ePolicy)

You will receive an email notification with your ePolicy contract attached, along with a secure link to access the same material via the My Sun Life Client Portal. This email will include detailed instructions to guide you through the process.

To ensure successful delivery via email, please provide a valid email address.

You may request a printed policy contract through any Client Service Center for a PHP 300 fee (for annual premium amount below P500,000.00)*.

You will need to submit the following:

- Request for Printing of Policy Contract form

- Valid ID of policy owner

- Proof of payment

The printed contract will be delivered either to your advisor’s branch or your preferred mailing address – provided a Special Delivery Form has been submitted beforehand.

Only eligible accounts may request a printed policy contract. These include individual life policies that:

- Have already received the digital (ePolicy) version

- Have not yet received a printed copy (Business and entity accounts are not included)

If you have already received a printed policy contract and require a replacement, please submit a completed Declaration of Loss form and pay a PHP 750 fee. For information on the available payment channel options, click here.

*Printing fee is free if annual premium amount is P500,000 and above.

You may print the ePolicy sent to your email address and My Sun Life Client Portal and save on printing costs and delivery fees.

A printed policy contract may only be requested once the digital version has been delivered via email and is accessible through the My Sun Life Client Portal. It cannot be requested or paid for during the application stage. The application must first be approved and settled before any request for a printed copy can be made.

Yes, ePolicy contracts are delivered significantly faster than printed versions. While printed policy contracts usually take 5 to 10 business days for delivery, digital contracts are sent via email and made available on the My Sun Life Client Portal shortly after approval. This not only shortens turnaround time but also enhances tracking and accessibility.

The printed policy contract will be delivered either to your Advisor’s branch or to your preferred mailing address – provided a Special Delivery Form has been submitted in advance.

General Questions

We are committed to protecting your privacy. We keep your financial and personal information confidential. Access to this information is restricted to authorized individuals who are responsible for the administration, processing, and servicing of your contract(s) with us. These may include select employees, advisors, third party service providers, and reinsurers.

Visit our website to know more about our Privacy Policy.

Please make sure that all details indicated in your policy contract are correct. If there is any error, inform us immediately so we can correct your policy records.

For all transactions and inquiries, always be ready with your policy number.

An authorized representative of an insurance company who sells and services insurance contracts.

Also referred to as financial advisor or insurance advisor.

Mutual Funds |

UITFs |

|

Subscription |

Funds are pooled by a group of investors and entrusted to a fund manager who will manage the funds among certain asset classes such as stocks, bonds, or a mix of both (i.e., balanced funds). |

|

Accounting/ Valuation/ Custody |

Securities may be valued under similar accounting standards (e.g., mark-to-market), and are entrusted to third-party custodians. |

|

Returns |

Unlike time deposits, neither products provide guaranteed returns. |

|

Structure |

Mutual funds are structured as a corporation, where each investor is the shareholder who is entitled to various rights given to shareholders (e.g., voting, participation in stockholders’ meetings). |

UITFs are contractual. Its investors (unitholders) and trustees (fund managers) are bound by a written contract that evidences an investor’s participation in the fund. |

Regulator |

Securities and Exchange Commission (SEC) |

Bangko Sentral ng Pilipinas (BSP) |

In a participating insurance policy, the premiums, death benefits and cash values are fixed and it is the Company that decides on where to invest the premiums. In a variable unit-linked policy, the death benefits and premiums are flexible and it is the Policy Owner who chooses where to invest his/her funds.

"

Variable unit-linked insurance (VUL) is an insurance policy with benefits directly linked to the performance of underlying funds. It is also called "variable universal life policy," "equity-linked policy" "investment-linked policy" or "variable unit-link policy".

Investing in a mutual fund is similar to investing in a company. You receive shares/units of participation in a mutual fund in exchange for the cash you contribute. Each share/unit has a specific value, referred to as the Net Asset Value Per Share (NAVPS)/Net Asset Value Per Unit (NAVPU).

The NAVPS/NAVPU is calculated daily at the end of every business day. This considers the income, gains, and losses of the securities your fund is invested in, so the price may change from day to day. You can calculate the fund’s NAVPS/NAVPU by dividing net assets (obtained by subtracting total liabilities from total assets) by the number of shares/units outstanding:

NAVPS/NAVPU = (Total Value of Fund Assets – Fund Liabilities) / Number of Outstanding Shares or Units

Fund Value is the total amount of money available in the funds that you selected. To get the fund value, multiply the outstanding units of each fund by their respective NAVPUs then add these together.

The Fund Value varies as NAVPUs fluctuate in value on each valuation date.

A dividend is an amount of money given to the Policy Owner of a participating insurance policy. It results when actual mortality, investment earnings, expenses, and other factors are more favorable than expected when premiums were set. Policy dividends are not guaranteed.

Only participating policies earn dividends.

A Policy Owner has the following options in using dividends:

If you are a participating Policy Owner, you have the following options on how to use your dividends:

- Paid-Up Addition - Dividends are used to purchase additional insurance coverage.

- Premium Reduction - Dividends are used to pay the current year/s premium. If the dividend is insufficient to pay the full year/s premium, you will be billed for the difference. If the dividend is in excess, this amount will be given to you in the form of check.

- Dividend Accumulation - Dividends are left with the Company to accumulate at the declared rate.

- Cash - Dividends are paid yearly to the Policy Owner in the form of check.

An anticipated endowment is a guaranteed cash benefit that is usually equivalent to a percentage of your face amount. This is paid out by the Company at intervals specified in your policy contract. Not all policies have this feature.

Example: Anticipated endowment = 20% of the Face Amount Payout schedule: Starting at the end of the second policy year and every two (2) years thereafter.

The person or entity named in the policy as the recipient of the policy's living or death benefit.

The amount payable by the insurance company to a claimant, assignee, or beneficiary.

The termination of insurance coverage.

For a participating insurance policy, it is the amount of money adjusted for factors such as policy advances or unpaid premiums that the Policy Owner will receive if he/she surrenders the policy to the insurance company.

For a variable life insurance policy, it is the amount of money calculated by multiplying the unit price of investment fund where the Policy Owner's funds are invested by the total number of units in said investment fund (i.e. unit price x total number of units) that the Policy Owner will receive if he/she surrenders the policy to the insurance company.

A policy that has been surrendered can no longer be reinstated.

For participating insurance policy, this is the amount available in cash upon surrender of a policy before it becomes payable upon death or maturity.

When the Policy Owner or beneficiary asks the insurance company to pay the benefits covered by the insurance policy.

The amount of money payable to the beneficiary upon death of the life insured.

This is the date when insurance coverage begins. This is also called issue date.

The Social Security System (SSS) is a state-funded system where all income earning members contribute monthly to the fund based on their salary range. The fund is then used for insurance benefits such as sickness, maternity, disability, retirement, death, and funeral expenses.

The Social Security System (SSS) provides insurance benefits such as sickness, maternity, disability, retirement, death, and funeral expenses to its members.

This is a type of insurance that pays out a sum of money either on the death of the insured person or after a set period.

Health insurance is also known as medical insurance. It provides coverage for hospitalization expenses and accidents. The full coverage will depend on your insurance policy. Please contact your advisor for the full details.

Insurance coverage is the amount of risk or liability that is covered for an individual or entity by way of insurance services.

Pre-existing conditions are health problems the insured has before a new health insurance policy coverage takes effect.

A critical illness is a type of disease that may require long-term hospitalization and recovery or may even result in the patient's demise.

Estate planning is the process of managing and disposing of an individual's assets in the event of their death or if he/she becomes incapacitated.

The person whose life is insured under the policy.

Cost of maintaining and administering the policy.

Anniversary of the policy's effective date.

Document which states all the benefits, terms and conditions of the policy.

Owner of a life insurance policy.

Payment for an insurance policy.

Cost of sales transaction and other expenses for the acquisition of a VUL policy.

These are annual, semi-annual or quarterly payments for a VUL policy. It consists of the basic and additional benefit premiums.

Lump-sum or one-time payment for an insurance policy.

A type of insurance policy that provides insurance coverage for a limited period as specified in the contract. This is not a participating policy.

Insurance Related Questions

This is the amount of coverage of an insurance policy. This is also called as "Sum Assured".

In most cases, the Face Amount is also the death benefit, but there are policies in which the death benefit is expressed as a certain percentage of the Face Amount.

E.g. Death Benefit = 200% of the Face Amount

The date on which the policy or its additional benefits end.

Charge for providing insurance coverage including any additional benefits.

Termination of coverage due to non-payment of premium.

These are options that allow the Policy Owner to keep the policy in-force despite nonpayment of premiums.

The following documents are required to withdraw your dividends:

- Duly-signed Dividend/Endowment Authorization Form

- Valid ID

A dividend option may be changed any time as long as your policy is in-force. Simply complete a Dividend/Endowment Benefit Authorization form.

Evidence of insurability may be required if you so desired that the existing dividend accumulation be applied as Paid-up Addition.

You may choose to receive your anticipated endowment benefits via:

Cash - a check will be sent to the endowment beneficiary/ies on record

Deposit - your endowment benefit are left with the company to accumulate

The following documents are required to withdraw your anticipated endowment benefits:

- Duly-signed Dividend/Endowment Authorization Form

- Valid ID

Yes. To change your anticipated endowment benefit option, submit a Dividend/Endowment Benefit Authorization form.

Yes. To change your anticipated endowment beneficiary, submit an Appointment/Change of Endowment Beneficiary form. Your new beneficiary will receive the endowment proceeds after the approval of such request. Endowment proceeds which were accumulated prior to approval will be given to your former beneficiary.

Statement or proof of physical condition and other factual information to support one's application for insurance, additional benefits, reinstatement, etc.

A type of insurance policy that earns dividends.

A type of insurance policy; with no dividends.

E.g. Term Insurance.

This is an amount borrowed from the policy's cash value at a specified interest rate. It can be repaid any time. Any unpaid advance plus interest will be deducted from the insurance benefit when it becomes payable.

The following documents are required for a policy advance:

- Application for Policy Advance signed by the following:

-Policy owner

-Irrevocable beneficiary/ies, if any

- Policy Contract

- Valid IDs of Policy Owner and irrevocable beneficiary/ies, if any

These are options that allow the Policy Owner to keep the policy in-force despite nonpayment of premiums.

Paid-Up Term Insurance - The cash value is used to purchase term insurance, which generally provides the same amount coverage as the original policy but for a shorter period depending on the cash value available.

As term insurance:

- Policy will no longer earn dividends

- All additional benefits will be cancelled

- Policy advance will not be allowed

- Policy surrender will not be allowed

Paid-Up Insurance - The cash value is used to purchase paid-up insurance, which provides coverage for the same period as the original policy but at a lower amount depending on the cash value available.

As paid-up insurance, the policy will have:

- Reduced coverage

- Lower dividends

- No more additional or supplementary benefits

Automatic Premium Advance (APA) - The cash value of your policy is used to pay for an unpaid premium. This is considered an advance subject to interest charges. You can check your policy contract for more details.

This is a premium payment default option in which the cash value is used to purchase term insurance with generally the same amount of coverage but for a shorter period.

This is a premium payment default option in which the cash value is used to continue the insurance policy keeping the original coverage period but at a reduced amount.

Mutual funds offer several levels of investor protection:

1. Mutual funds are regulated by the Securities and Exchange Commission (SEC) of the Philippines.

2. Every mutual fund corporation has a Board of Directors to whom it reports and whose primary duty is to protect investors' interests.

3. Mutual fund securities are held by reputable custodian banks and do not form part of the assets of the company managing the fund. The purpose of having custodians is to safekeep the documents that prove ownership of the Funds' assets.

For settled transactions starting July 15, 2025, all sales loads, whether front-end or back-end, are waived. Holding period and redemption fees for these transactions are also removed. Click HERE to know more.

For the following fees, these are already imputed in the Funds’ daily price (Net Asset Value Per Share / Net Asset Value Per Unit):

- Management and Distribution Fees

- Transfer Agency Fees

- Custodianship Fees

- Fund Accounting Fees

- Other Fees

Additional investments are not a requirement. However, we strongly advise our investors to regularly set aside a fixed amount of money for investments, regardless of the price or market condition. This way, you can reduce your overall investment cost as you get more shares/units when prices are low, offsetting periods that give you fewer shares/units when prices are high. This kind of discipline is called Peso Cost Averaging.

If you wish to increase your investment in the funds, the minimum amount for additional investment is PHP 1,000 for the Philippine Peso-denominated funds* and USD 100 for the US Dollar denominated funds, regardless of the sales load option (front-end or back-end).

If you are interested to enjoy the benefits of Peso-Cost Averaging, you may explore our Auto-Invest facility.

*Except for the Sun Life Prosperity Peso Starter Fund (formerly Money Market Fund) and Sun Life Prosperity World Equity Index Feeder Fund, which have minimum additional investment amounts of only PHP 100 and PHP 10,000 respectively.

Here are the different ways you can add to your mutual fund investments:

Through Sun Life channels

- My Sun Life Client Portal

- Sun Life PH Mobile App

- Sun Life Online Payment Page

- Sun Life Prosperity Card

- Sun Life Client Service Center (via Cash Deposit Machine or over-the-counter; you can also view our list of Sun Life Client Service Centers)

Through bank partners

- Bills Payment Facility (electronic or over-the-counter)

- Auto-Invest Facility

- Local Bank Deposit

Visit the Mutual Fund Payment Channels

Mutual funds serve as alternatives to investing directly in the stock market. Compared to buying stocks directly, mutual funds require lower investment amounts while allowing you to achieve diversification. This means that for a small amount of money, you can buy into several companies and achieve variety for your portfolio. When buying stocks directly, a larger amount of capital may be required to achieve the same level of diversification.

Investing in mutual funds like the Sun Life of Canada Prosperity Philippine Equity Fund (“Equity Fund”) also allows you to benefit from the expertise of fund managers who perform the stock selection for you.

To compute for the number of shares or units bought, we divide the investment amount by the Offering Price, which is equivalent to the NAVPS/NAVPU plus the applicable sales charge:

Number of Shares/Units Bought = Amount of Investment / Offering Price

Forward pricing is the way in which investments like mutual funds are valued for investors who bought or redeemed (sold) their shares/units. The applicable NAVPS/NAVPU (Offering Price) used to price these shares/units is only determined at the end of every business day when all orders are in and markets have closed.

This means that you do not know the purchase or redemption price until the next business day. This is because the price of a mutual fund will remain static throughout market hours. But when markets close, the closing market prices of each of its underlying assets will determine the mutual fund’s end-of-day price.

The decline of the local market, specifically the local stock exchange, is not exactly bad for mutual funds. In fact, this is the ideal time to buy stocks for mutual funds, when the prices are low. When the market improves and share prices go up, as they will, given time, the value of the equity securities will have risen along with them. Mutual funds are long-term investments, which should not be bought or sold based on short-term events.

Returns are not guaranteed. However, based on historical experience, stocks, and equity funds in particular, tend to go up in value over time for investors who are prepared to buy and hold for the long-term. Do note though that past performance is not an indicator of future returns.

Yes, but while you will bear the risk of investing in your chosen fund, it will also give you an opportunity to take advantage of potential returns.

Should you need guidance in investing, your Sun Life Mutual Fund Advisor is always ready to assist you.

Generally, the rates of return in an investment cannot be guaranteed, and a mutual fund is a type of investment that is designed to be held in the long-term in order to achieve potentially high returns.

Moreover, when you invest in a mutual fund, you are investing in a diversified portfolio of securities that normally fluctuate in value. The markets in which mutual funds invest in tend to rise and fall over the short-term, as will the value of your investment. This is also why past mutual fund performance does not guarantee future performance.

Sun Life, through its subsidiaries worldwide, has been managing mutual funds for several decades. In fact, the oldest mutual funds in the United States and Canada are managed by members of the Sun Life group of companies.

Locally, a seasoned team of investment professionals handles the investment management of our funds.

Step 1: Accomplish a Request for Redemption / Fund Switch Form available here.

Step 2: Select your preferred Settlement Details (choose one) from the Request for Redemption/Fund Switch Form:

- Deposit to Bank / Credit to Account*

- Switch to another fund

- Payment for Sun Life Policies

- Pick up check at Client Service Center (CSC)

* We highly encourage you to use Deposit to Bank/Credit to Account Redemptions for faster and more secure crediting. Please fill out field 9b of the form where you can enroll a Settlement Bank Account and submit Proof of Bank Account Ownership (PBAO) as a requirement.

To know more about enrolling your Settlement Bank Account, please read the SBA FAQ.

Step 3: Submit scanned copy of the signed Request for Redemption / Fund Switch Form and supporting documentation (as needed) to requestslamci@sunlife.com.

Step 1: Accomplish a Request for Redemption/Fund Switch Form available at https://sunlife.co/Fund-Redeem-Switch

Step 2: Select your preferred Settlement Details (choose one) from the Request for Redemption / Fund Switch Form:

- Deposit to Bank / Credit to Account*

- Switch to another fund

- Payment for Sun Life Policies

- Pick up check at Client Service Center (CSC)

* We highly encourage you to use Deposit to Bank/Credit to Account Redemptions for faster and more secure crediting. Please fill out field 9b of the form where you can enroll a Settlement Bank Account and submit Proof of Bank Account Ownership (PBAO) as a requirement.

To know more about enrolling your Settlement Bank Account, please read the SBA FAQ.

Step 3: Bring a printed copy of the signed Request for Redemption/Fund Switch Form with supporting documentation (as needed) and go to a Sun Life CSC Branch near you.

Client Portal |

Mobile App |

1. Login to your Sun Life Client Portal |

1. Login to your Sun Life Mobile App |

2. Go to Mutual Funds |

2. Go to Mutual Funds |

3. Select an Account and click the Redeem fund button. |

3. Select an Account and click the Redeem fund button. |

4. Fill out the details and select your preferred Redemption Options below,

*For “Credit to new bank account for enrollment”, you are required to enroll a Settlement Bank Account (SBA) by entering your bank details and Upload Proof of Bank Account Ownership (PBAO). **Select “Credit to enrolled bank account” ONLY if you already have an enrolled Settlement Bank Account. |

4. Fill out the details and select your preferred Redemption Options below,

*For “Credit to new bank account for enrollment”, you are required to enroll a Settlement Bank Account (SBA) by entering your bank details and Upload Proof of Bank Account Ownership (PBAO). **Select “Credit to enrolled bank account” ONLY if you already have an enrolled Settlement Bank Account. |

5. Click the Submit button. |

5. Click the Proceed button. |

6. An OTP will be sent to your enrolled mobile number. OTPs for Redemption requests in CPMA is sent via SMS to your enrolled mobile number for security purposes |

6. An OTP will be sent to your enrolled mobile number. OTPs for Redemption requests in CPMA is sent via SMS to your enrolled mobile number for security purposes |

7. Input OTP to redeem your shares. |

7. Input OTP to redeem your shares. |

8. Your Order ticket number pops-up in the screen and an email notification of the redeem request will be sent |

8. Your Order ticket number pops-up in the screen and an email notification of the redeem request will be sent |

Note: If you update your mobile number or email address through the My Sun Life Client Portal and Mobile App, there will be a 24-hour Redemption Pause window before you can redeem your MF shares through these two channels. This is to protect our clients from unauthorized redemptions.

The number of days it takes for redemptions to be processed depends on your Fund’s redemption turnaround time.

Peso Starter and Dollar Starter Funds |

Transaction Date (T) + 1 business day |

GS and Bond Funds |

T + 2 business days |

| Balanced, Achiever (2028, 2038, and 2048), Index, and Equity Funds | T + 3 business days |

Dollar Abundance, Dollar Wellspring, Dollar Advantage, and World Voyager Funds |

T + 4 business days |

World Equity Index Feeder Fund |

T + 5 business days |

For example, our Equity Fund follows a redemption turnaround time of T + three (3) business days. This means that if you place your redemption order on a Monday before our daily cut-off time, your redemption proceeds from the fund will be priced based on the applicable end-of-day NAVPS on Monday and will be credited to your settlement account on Thursday. When determining the settlement date, however, please do not include weekends and non-working holidays.

The value of the redemption proceeds you will receive will be based on the applicable Net Asset Value per Share (NAVPS)/Net Asset Value per Unit (NAVPU) on the day your transaction was processed.

You can enroll your preferred SBA during any of these transactions:

1. When redeeming from your funds (during fund redemption)

- via Forms

- via the Sun Life Client Portal and Mobile App

2. When opening an investment account

3. Stand-alone request (anytime, on-demand)

Enrollment of Settlement Bank Account (SBA) and submission of Proof of Bank Account Ownership (PBAO) are required for all credit-to-account redemption transactions.

Fund redemption via Forms:

Step 1: Accomplish the Request for Redemption/Fund Switch Form available here.

Note: For Credit-to-Account redemptions, please fill out 9b of the form.

Step 2: Submit a clear copy of Proof of Bank Account Ownership (PBAO) and a valid ID. PBAO can be any one (1) of the following:

- Bank Statement of Account

- Certificate of Bank Deposit

- First page of Bank Passbook

- Cheque

- ATM Card showing the Bank Account

- Machine-validated Deposit Slip

- Machine-validated Withdrawal Slip

Note:

PBAO must clearly show the complete bank account number and account name on one (1) page. Kindly refrain from providing sensitive data such as bank balances and personal information as these are not required in the enrollment of SBA.

The Valid ID should have a signature matching the signature in the accomplished forms.

Step 3: Submit the printed copies to a CSC branch near you OR submit a scanned copy to requestslamci@sunlife.com following SLAMCI’s updated DES guidelines.

Fund redemption via the Sun Life Client Portal and Mobile App:

Client Portal |

Mobile App |

1. Login to your Sun Life Client Portal |

1. Login to your Sun Life Mobile App |

2. Go to Mutual Funds |

2. Go to Mutual Funds |

3. Select an Account and click the Redeem fund button. |

3. Select an Account and click the Redeem fund button. |

4. Fill out the details and select “Credit to new bank account for enrollment” as your preferred Redemption Options. Please select “Credit to enrolled bank account” ONLY if you already have an enrolled Settlement Bank Account. |

4. Fill out the details and select “Credit to new bank account for enrollment” as your preferred Redemption Options. Please select “Credit to enrolled bank account” ONLY if you already have an enrolled Settlement Bank Account. |

5. Upload Proof of Bank Account Ownership (PBAO) Format limitation: 10MB limit, jpg, png only |

5. Upload Proof of Bank Account Ownership (PBAO) Format limitation: 10MB limit, jpg, png only |

5. Click the Submit button. |

5. Click the Proceed button. |

6. An OTP will be sent to your enrolled mobile number. OTPs for Redemption requests in CPMA is sent via SMS to your enrolled mobile number for security purposes |

6. An OTP will be sent to your enrolled mobile number. OTPs for Redemption requests in CPMA is sent via SMS to your enrolled mobile number for security purposes |

7. Input OTP to redeem your shares. |

7. Input OTP to redeem your shares. |

8. Your Order Ticket Number pops-up in the screen and an email notification of the redeem request will be sent |

8. Your Order Ticket Number pops-up in the screen and an email notification of the redeem request will be sent |

Note: If you update your mobile number or email address through the My Sun Life Client Portal and Mobile App, there will be a 24-hour Redemption Pause window before you can redeem your MF shares through these two channels.This is to protect our clients from unauthorized redemptions.

To know more about enrolling your Settlement Bank Account, please read the SBA FAQ.

Step 1: Accomplish the Account Opening Form (Individual / Institution) available below

- https://sunlife.co/AOF-individual for individual accounts

- https://sunlife.co/AOF-Institutions for institutional accounts

Note: For nominated SBA, please fill out Section F for individual accounts, and Section D for institutional accounts.

Step 2: Submit a clear copy of PBAO & Valid ID. PBAO can be any one (1) of the following:

- Bank Statement of Account

- Certificate of Bank Deposit

- First page of bank passbook

- Cheque

- ATM card showing the Bank Account

- Machine-validated Deposit Slip

- Machine-validated Withdrawal Slip

Note:

PBAO must clearly show the complete bank account number and account name on one (1) page. Kindly refrain from providing sensitive data such as bank balances and personal information as these are not required in the enrollment of SBA.

The Valid ID should have a signature matching the signature in the accomplished forms.

Step 3: Submit the printed copies to a CSC branch near you OR submit a scanned copy to requestslamci@sunlife.com following SLAMCI’s updated DES guidelines.

To know more about enrolling your Settlement Bank Account, please read the SBA FAQ.

Step 1: Accomplish the Settlement Bank Account Enrollment Form (New Form) available at https://sunlife.co/EnrollMySBA

Step 2: Submit a clear copy of PBAO & Valid ID. PBAO can be any one (1) of the following:

- Bank Statement of Account

- Certificate of Bank Deposit

- First page of bank passbook

- Cheque

- ATM card showing the Bank Account

- Machine-validated Deposit Slip

- Machine-validated Withdrawal Slip

Note:

PBAO must clearly show the complete bank account number and account name on one (1) page. Kindly refrain from providing sensitive data such as bank balances and personal information as these are not required in the enrollment of SBA.

The Valid ID should have a signature matching the signature in the accomplished forms.

Step 3: Submit the printed copies to a CSC branch near you OR submit a scanned copy to SLAMC@sunlife.com following SLAMCI’s updated DES guidelines.

To know more about enrolling your Settlement Bank Account, please read the SBA FAQ.

Orphaned Clients

Lost contact with your Sun Life Advisor? Want someone more aligned with your needs? Here’s everything you need to know about requesting a replacement.

There are five ways to request a new Sun Life Advisor:

Via email

Simply submit an Advisor Change Request via sunlink@sunlife.com. You should hear back from us in 24 hours.

Via Sun Cares

- Visit Sun Cares

- Under Your feedback is about, select Feedback about my Advisor

- Under Your specific concern is, select Change or request for a new Advisor

- Fill out the form

- Agree to the Privacy Statement, then click Submit

You should receive a response from us in 24 hours.

Via phone

Please call Client Care at (632) 8849 9888

In person

Please visit the nearest Sun Life Client Service Center.

Note: If we’ve confirmed that your Advisor is no longer with Sun Life, we’ll notify you via email and SMS that we will be assigning you a replacement within 15 business days. You’ll be able to confirm your new Advisor’s details under Policy information on the My Sun Life PH Client Portal and Mobile App.

A new Advisor should be assigned to you within 15 business days. If you don’t hear from us within this period, please get in touch via Client Care for assistance:

- (632) 8849 9888

- sunlink@sunlife.com

Alternatively, you can file an advisor change request.

Via email

Simply submit an Advisor Change Request via sunlink@sunlife.com. You should hear back from us in 24 hours.

Via Sun Cares

- Visit Sun Cares

- Under Your feedback is about, select Feedback about my Advisor

- Under Your specific concern is, select Change or request for a new Advisor

- Fill out the form

- Agree to the Privacy Statement, then click Submit

You should receive a response from us in 24 hours.

Via phone

Please call Client Care at (632) 8849 9888

In person

Please visit the nearest Sun Life Client Service Center.

You can view your Advisor’s details under Policy information on the My Sun Life PH Client Portal and Mobile App.

If you still wish to request a new Sun Life Advisor, you have five options:

Via email

Simply submit an Advisor Change Request via sunlink@sunlife.com. You should hear back from us in 24 hours.

Via Sun Cares

- Visit Sun Cares

- Under Your feedback is about, select Feedback about my Advisor

- Under Your specific concern is, select Change or request for a new Advisor

- Fill out the form

- Agree to the Privacy Statement, then click Submit

You should receive a response from us in 24 hours.

Via phone

Please call Client Care at (632) 8849 9888

In person

Please visit the nearest Sun Life Client Service Center.

There are five ways to request a new Sun Life Advisor:

Via email

Simply submit an Advisor Change Request via sunlink@sunlife.com. You should hear back from us in 24 hours.

Via Sun Cares

- Visit Sun Cares

- Under Your feedback is about, select Feedback about my Advisor

- Under Your specific concern is, select Change or request for a new Advisor

- Fill out the form

- Agree to the Privacy Statement, then click Submit

You should receive a response from us in 24 hours.

Via phone

Please call Client Care at (632) 8849 9888

In person

Please visit the nearest Sun Life Client Service Center.

You can share feedback about your Sun Life Advisor via Sun Cares.

- Visit Sun Cares

- Under Your feedback is about, select Feedback about my Advisor

- Under Your specific concern is, choose either Happy with Advisor or Unhappy with Advisor

- Fill out the form

Agree to the Privacy Statement, then click Submit.

Yes. You can manage your policies and accounts yourself via the My Sun Life PH Client Portal or Mobile App.

Paperless Subscription

The paperless initiative aims to deliver policy notifications more securely and to help reduce deforestation and energy use related to paper production.

Once enrolled, you will receive policy notifications electronically via your registered email address and mobile number.

A valid email address is required to enroll in eSubscription and be able to access your electronic policy notifications anytime, anywhere. Contact us at sunlink@sunlife.com or Client Care at (632) 8849-9888 for assistance.

We strongly encourage Clients to register to the Client Portal or Mobile App for the most convenient and secure way of viewing their policies and manage communications. However, if you are unable to register at this time, you will continue to receive Paper Billings and Notices delivered to your registered mailing address. Please make sure your address is up-to-date to avoid delay in delivery.

You may request to update your contact information and mailing address by:

- Requesting assistance from your Advisor

- Sending an email to sunlink@sunlife.com

- Calling us at Client Care (+632) 8849-9888

Yes, you will receive email and SMS notifications when your Advisor makes changes to your subscription preferences.

To make sure your get these updates, please keep your contact details up to date. Here's how you can update your email address and mobile number:

If you're an existing Sun Life PH app user, you can update your contact information through your Client Portal and Mobile App account.

{kind=link}

{kind=link}

If you're not yet registered, you may:

- Request assistance from your Advisor

- Send an email to sunlink@sunlife.com

- Call us at Client Care at (+632) 8849-9888

You just need to enroll through Manage eSubscriptions through the My Sun Life PH Client Portal. Make sure your email address and mobile number are updated and active.

Here's how:

- Click here or go to sunlife.com.ph and click the "Log in" button on the upper right side.

- After signing in, click "Settings" on the left side of your dashboard. Select "Account Management" from the tabs and click on "Notification Settings".

- Select "SMS and My Sun Life Client Portal (eNotice)" and "SMS and My Sun Life Client Portal (eOR)" to receive billing notices and receipts electronically.

- If left unchecked, you won't see these notices and receipts on your dashboard, and they will not be sent to your email or mobile number.

- Click “Update” if you agree to receive billing notices and receipts via your dashaboard, email, and SMS.

No, once enrolled in eSubscriptions, you'll start receiving your policy notices and invoices by email and SMS beginning with your next billing cycle. You will no longer receive printed copies by mail.

If you prefer paper communications, you may request to switch off eSubscriptions by:

- Requesting assistance from your Advisor

- Sending an email to sunlink@sunlife.com

- Calling us at Client Care (+632) 8849-9888

However, we really encourage eSubscriptions for your convenience such as faster delivery, improved security and to also help in our sustainability efforts.

Yes. Digital notices are sent to your registered email address and mobile number and are password-protected when needed to ensure your personal and policy information stays secure.

You’ll receive an SMS and email notification when a new billing notice or document is available.

Please ensure your email and mobile number are up to date in your client profile. Also, regularly check your spam or junk folder to avoid missing important messages.

Once enrolled to eSubscriptions, you will begin receiving the following documents via email or through the My Sun Life Client Portal website:

- Policy Notices (eNotice)

- Billing Invoices (eInvoice)

For now, these are the primary documents available digitally. More types of notices may be added in the future as we continue to enhance our digital services.

Payment

Due dates? Payment channels? Grace periods? Here’s everything you need to know about paying for your Sun Life policy.

If you’re in the Philippines, you can pay your insurance premiums through any of the following channels:

- My Sun Life PH Client Portal and Mobile App

- Sun Life Online Payment

- Online and over-the-counter bills payment via banks

- Digital payment channels (GCash, Maya, Smart Money, Bayad PH)

- Auto charge and auto debit arrangement

- Payment centers

- Local bank deposit (for initial payments only)

- Sun Life Client Service Center over-the-counter payment

If you’re overseas, you can pay via:

- Wire transfer to any of our authorized collecting bank partners

- Overseas banks (PNB Overseas Remittance Center, BDO Kabayan Bills Bayad, and Telepay for RCBC Remittance

- Overseas Sun Life offices (USA, Canada, and Hong Kong)

Please note that any applicable charges and bank fees will be charged to your account. For more information, please visit the life insurance payment channels page.

You should pay your insurance premiums on or before the due date specified in your policy contract.

If you miss a due date, you can keep your policy from lapsing by paying within the 31-day grace period*. We will send you reminders to help you keep track of any overdue payments more easily.

Want to go paperless and receive your notices online? You can do so via any the following channels:

My Sun Life PH Client Portal

- Go to sunlife.com.ph and click the "Log in" button on the upper right side.

- After signing in, click "Settings" on the left side of your dashboard. Select "Account Management" from the tabs and click on "Notification Settings".

- Select "SMS and My Sun Life Client Portal (eNotice)" and "SMS and My Sun Life Client Portal (eOR)" to receive billing notices and receipts electronically.

If left unchecked, you won't see these notices and receipts on your dashboard, and they will not be sent to your email or mobile number. - Click “Update” if you agree to receive billing notices and receipts via your dashaboard, email, and SMS.

Your Sun Life Advisor

Simply let your Advisor know about your request.

Client Care

Please call (632) 8849 9888 or send an email to sunlink@sunlife.com.

Sun Life Client Service Center

Please visit the nearest Client Service Center

Note: We will no longer send you printed copies of your notices once you opt in to receive digital copies.

*For VUL plans, the grace period ends once the fund value is no longer enough to cover the monthly charges.

Yes, you can make advance payments.

If you’re in the Philippines, you can pay through any of the following channels:

- My Sun Life PH Client Portal and Mobile App

- Sun Life Online Payment page

- Online and over-the-counter bills payment via banks

- Digital payment channels (GCash, Maya, Smart Money, Bayad PH)

- Auto charge and auto debit arrangement

- Payment centers

- Local bank deposit (for initial payments only)

- Sun Life Client Service Center over-the-counter payment

If you’re overseas, you can pay via:

- Wire transfer to any of our authorized collecting bank partners

- Overseas banks (PNB Overseas Remittance Center, BDO Kabayan Bills Bayad,, and Telepay for RCBC Remittance

- Overseas Sun Life offices (USA, Canada, and Hong Kong)

Please note that any applicable charges and bank fees will be charged to your account. For more information, please visit the life insurance payment channels page.

Advanced payments get credited on your next premium due date. You can get a discount by enrolling under Advance Payment Option. To know more, please contact us via any of the following channels:

- (632) 8849 9888

- sunlink@sunlife.com

- The nearest Sun Life Client Service Center.

You may pay through any of the following:

- My Sun Life Client Portal and Sun Life PH mobile app

- Online and over-the-counter bank bills payment

- Paymaya

- Gcash

- Auto charge and auto debit arrangement

- Payment centers

- Local bank deposit (for initial payments only)

- Overseas banks

- Sun Life Client Service Center - Cash Deposit Machine

- Sun Life Client Service Center over-the-counter payment

- Overseas Sun Life Offices

Read more details about life insurance payment channels.

You may pay your premiums through any of the following channels:

- Wire transfer to any of our authorized collecting bank partners (please refer to the list of our collecting over-the-counter overseas banks).

- PNB Overseas Remittance Center

Applicable charges and bank fees will be on your account.

Yes, you can make advance payments.

If you’re in the Philippines, you can pay through any of the following channels:

- My Sun Life PH Client Portal and Mobile App

- Sun Life Online Payment page

- Online and over-the-counter bills payment via banks

- Digital payment channels (GCash, Maya, Smart Money, Bayad PH)

- Auto charge and auto debit arrangement

- Payment centers

- Local bank deposit (for initial payments only)

- Sun Life Client Service Center over-the-counter payment

If you’re overseas, you can pay via:

- Wire transfer to any of our authorized collecting bank partners

- Overseas banks (PNB Overseas Remittance Center, BDO Kabayan Bills Bayad,, and Telepay for RCBC Remittance

- Overseas Sun Life offices (USA, Canada, and Hong Kong)

Please note that any applicable charges and bank fees will be charged to your account. For more information, please visit the pre-need payment channels page.

If you fail to pay the regular premiums due on your VUL policy, the policy will continue to be in-force provided the Fund Value is sufficient to cover the Monthly Periodic Charges and Insurance Charges. However, we encourage you to pay your premiums on time so that the Fund Value will continue to grow and you may achieve your financial goals.

This is the period of time that the Policy Owner is still allowed to pay and keep the policy in-force when payment is missed on the premium due date. For a VUL policy, this is the period when the fund value is no longer sufficient to cover monthly charges.

The grace period is the period of time where you’re allowed to settle any overdue premium payments without your policy lapsing. For most policies, it’s 31 days. For VUL plans, it ends once the fund value is no longer enough to cover the monthly charges.

The extended grace period, on the other hand, keeps your VUL plan active even after its fund value is exhausted as long as:

- Your VUL plan is still within its first year

- You pay your regular premiums on or before the due date

The total amount of your withdrawals is not higher than the total excess premiums you paid

Payments usually get credited either on the same day or the next business day, depending on the payment method you use.

For overseas payments, crediting may take 3–5 business days.

Excess premiums are additional premiums that you may use to increase your life insurance coverage and investments. On top of your regular or single premium, excess premiums are used to purchase additional units of your chosen fund resulting in an increase in policy benefits.

Excess Premiums can be a one-time payment or these can be billed regularly together with your regular premiums. These may require evidence of insurability.

Also known as excess premiums, top-ups are optional additional premiums you can pay to buy additional units of your VUL plan’s linked funds, resulting in:

- Increased policy benefits

- Improved investment earning potential due to the increased number of units

Top-ups can either be a one-time payment or billed regularly along with your regular premiums. They may also require evidence of insurability.

If you miss a premium payment, you can still keep your policy from lapsing by paying within the 31-day grace period*. Please note that if your policy does end up lapsing, you will lose all its benefits.

*For VUL plans the grace period ends once the fund value is no longer enough to cover the monthly charges.

You can pay your policy advance (loan) anytime or request a repayment schedule from us via any of the following channels:

- (632) 8849 9888

- sunlink@sunlife.com

Policy Service Questions

You can access your policy information conveniently through various Sun Link Systems:

Client Portal

Manage your account and access policy information by registering in the My Sun Life client portal. Learn how to register and download the Sun Life PH mobile app.

Client Care

- (632) 8849-9888

- Domestic Toll Free 1-800-10-SUNLIFE (7865433) using a PLDT Line

E-mail Address

- sunlink@sunlife.com

Website

- www.sunlife.com.ph

You may also visit any of our Client Service Centers. For your protection, we will require you to present two (2) original, government-issued, photo-bearing valid IDs (i.e. not expired), and/or answer questions to establish your identity.

Here are the different changes that may be applicable to a policy. Check your contract to know which ones are applicable to yours:

- Reduction/Increase in Coverage

- Correction of Birthdate/Sex

- Addition/Deletion of Riders

- Change from Smoker to Non-Smoker Rate

- Removal of extra rating due to Occupation/Hobby/Medical

- Change in Mode of Payment

- Change in Mailing Address

- Transfer of Ownership

- Assignment of Policy as Collateral

- Conversion of Term Plan to Participating Plan

- Fully Paid-Up/Reduced Paid-Up Life/Paid-up Term

- Change of Plan

- Change in Premium Payment Default Option

- Change in Fund Allocation /Switch in Fund Allocation

Note: Forms are available from our online Find a Form page and Client Service Centers.

Name Change Request and Change Beneficiary forms (c/o Claims and Titles) ;Original or certified true copy of the legal document supporting your correct/new name (E.g. birth certificate, marriage contract, adoption papers) ;Valid ID

Please submit any of the following:

- Back portion of the premium notice

- Letter of request with signature

- Address and Contact Information Change Request form

Access your required forms in our Find a Form page.

Alternatively, you may update your contact information through the My Sun Life Client Portal or the Sun Life PH mobile app. Learn how to register to the My Sun Life Client Portal and download the Sun Life PH mobile app.

Title changes refer to changes relating to names, titles, relationships, beneficiary/ies among others.

Your VUL policy provides a cooling-off period that allows you to cancel it fifteen (15) days from the time you receive your policy contract.

If you cancel your VUL policy within the cooling-off period, you will get the Fund Value plus all initial charges. After the cooling-off period, you will receive the Fund Value less applicable surrender charge.

A VUL policy cannot be converted to a participating insurance policy.

You may place investments in the Sun Life Prosperity Funds under your name in trust for your child. Simply fill-out and indicate in the application form that the account is "in trust for" (ITF) the name of the child and accomplish a Confirmation of Trust agreement, available upon request from our Investor Services Department. Make sure that you provide a photocopy of your child's birth certificate when placing investments under an ITF account. However, please note that the investment will not automatically be placed under the name of the child, when he/she reaches the age of majority. A written request must come from you in order for the transfer to take effect.

The living benefits will be paid to you as the Policy Owner unless you sign a Waiver of Benefit Form during new business application. If such waiver is signed, living benefits will be paid to the life insured.

Reinstatement is the process of putting your policy back to active or "in-force" status.

The reinstatement provision differs according to each contract. Please refer to your contract for more information. You can also reach out to your Sun Life Financial Advisor for more information or contact us.

To reinstate your insurance policy, you will need:

- Reinstatement Form

- Reinstatement cost

- Evidence of insurability, as may be required

- Valid ID

You may assign your life insurance policy contract as collateral security to your creditor (i.e. a bank if you apply for a mortgage loan) by submitting the following:

- Assignment as Collateral Security Form signed by the Policy Owner and the irrevocable beneficiary/ies, if any

- Valid IDs of the Policy Owner and irrevocable beneficiary/ies, if any

After you have completed your mortgage payment, submit a Release of Assignment as Collateral Security Form duly signed by your assignee to update your policy records.

Requirements:

If assignee is an individual

- Assignee's signature on the form

- Assignee's valid ID

If assignee is an institution (i.e. bank or company)

- Signature of two (2) authorized signatories

- One (1) valid ID per authorized signatory

- Original copy or Certified True Copy of the Corporate Secretary's Certificate

- authorizing the signatories to sign on behalf of the Institution; and,

- approving the release of the assignment of the policy contract

You may transfer the ownership of your policy to another person or entity by submitting the following:

- Absolute Assignment for Value Form signed by the Policy Owner and the irrevocable beneficiary/ies, if any

- Valid ID of the Policy Owner and irrevocable beneficiary/ies, if any, and new Policy Owner

Note: Transfer of ownership between spouses is not permitted by law.

If you keep your policy in-force for at least ten (10) years, you may be entitled to a loyalty bonus in the form of additional units at the end of the 10th policy year and every five (5) years thereafter. The amount of bonus, which depends on the actual performance of the fund, is determined by the Company from time to time but is currently set at 2% of the average monthly fund balance of the preceding past five (5) years.

Your policy will be terminated and you will lose the insurance protection. Once surrendered, the policy may no longer be reinstated.

You will receive the guaranteed value of your policy plus any dividend less any policy advances with interest. Payment of this amount terminates the policy.

The following documents are required if you wish to surrender your policy:

- Cash Surrender Value Form signed by the Policy Owner and the irrevocable beneficiary/ies, if any

- Policy contract

- Valid IDs of Policy Owner and irrevocable beneficiary/ies, if any

SIM Card Registration

As your SIM card will be deactivated by your carrier, the following may happen:

- You will not receive important notifications about your Sun Life accounts, such as updates on your claims or One-Time Passwords (OTPs) that are needed for online transactions.

- Transactions where recording the call is mandatory may be affected.

- Transactions might not push through as your mobile number has been deactivated. One example would be mutual fund transactions done via the app, as this requires an OTP which is sent via SMS.

- Your Sun Life advisor may not be able to reach you for essential updates regarding your account.

Your accounts will remain safe with us. However, for transactions that will require an OTP, you will first need to ensure that your mobile number has been registered and reactivated by your carrier.

Yes, you may still access your account via the Client Portal or Mobile App, so long as your username and password are still valid.

Once you log in, you may update your mobile number and email address. Moreover, under Personal Details, you may also opt to receive an OTP through your registered email address.

Simply update your records with us through any of the following channels:

- Call Sunlink Client Care at +632-8849-9888. Your contact information will be updated in our records in real time.

- Send an email to sunlink@sunlife.com. Your contact information will be updated in our records within 48 hours.

- Log in to your Client Portal or Mobile App account. Go to sunlife.co/portal, then use the Edit feature to change your email address, mobile number, or mailing address. You can also overwrite it with the same info and click proceed. Rest assured that your details will be updated in our records within 24 hours.

VUL Related Questions

A unit represents your ownership in the fund and is used to determine the fund value at any given point throughout the duration of your policy.

NAVPU is the value of each unit of the fund and is computed every valuation date. It is the basis for buying and selling units. It is also called unit price.

The fund in which one's premiums are invested in a VUL policy.

Your premiums (net of premium charges) will be invested after receipt of payment. For check payments, premiums will be invested after clearing.

The date on which the net asset value of the investment fund of a VUL policy is determined.

Percentage of premium to be invested in the VUL funds chosen by the Policy Owner.

You may change the fund allocation of your policy. Fund allocation is the percentage of your premium (after deducting the premium charge) that will be allocated to buy units in each of the funds you have chosen. You may change your policy's fund allocation in two (2) ways:

- Change the percentages to be allocated in each of the funds you have chosen; and/or

- Change the fund where you will buy units

You may change your fund allocation for free up to four (4) times within a policy year. You will be charged ₱750 if you exceed the limit.

The number of times you can change your fund allocation for free and the fixed amount to be charged when you exceed the limit may change subject to the approval of the Insurance Commission.

The following are the requirements:

- VUL Request for Policy Change Form signed by the following:

- Policy Owner / Assignee

- Irrevocable Beneficiary/ies (if any)

- Witness

- Valid ID

Premium charge is the cost associated with the policy's sales transaction and other related expenses.

Monthly Periodic Charge is the cost of maintaining and administering the policy.

Cost of Insurance Charge is the cost of insurance coverage and other additional benefits

VUL Withdrawal Questions

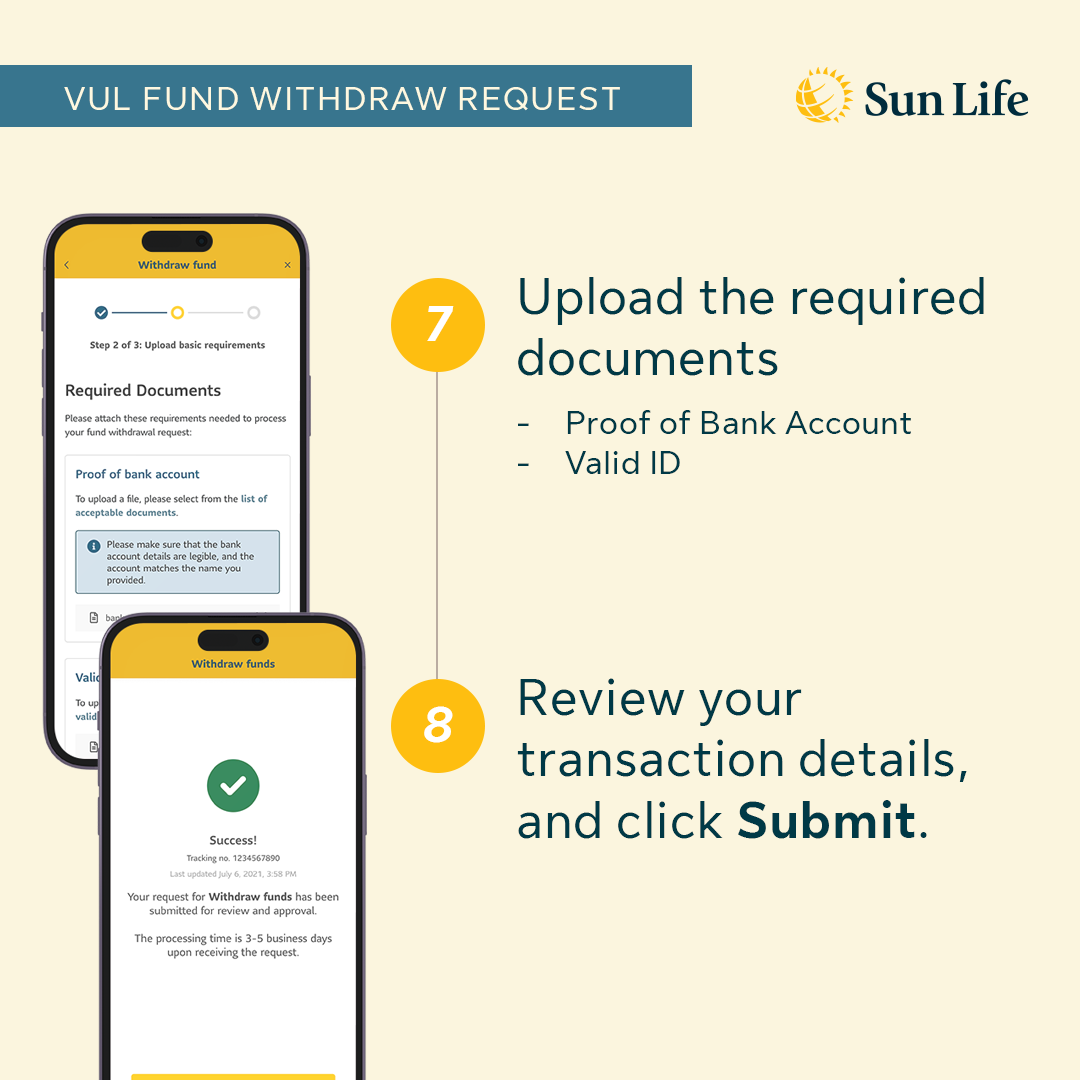

Individual policyowners of VUL policies may use the VUL fund withdrawal feature in the mobile app. Note that this applies only to VUL policies with revocable beneficiaries and that withdrawals can only be done while in the Philippines.

Step 1: Log in to your Sun Life PH Mobile App.

App Name: PH Sun Life on iOS / Sun Life PH on Android

Step 2: Click on Service Request tab at the bottom.

Step 3: Select Withdraw from my VUL.

Education Page: Please allow 5 business days for your request to be processed. We discourage withdrawal of the full amount. The amount projected is only an estimation and is subject to change due to Value Price and Admin Charges.

Step 4: Select the VUL policy to withdraw from.

Step 5: Enter the amount you’d like to withdraw.

Note: Some policies may incur admin charges

Step 6: Provide the bank account details where the funds will be credited.

Step 7: Upload the required documents.

There is an option to upload an existing document in your phone or take a photo of the document.

Please ensure that the file uploaded is in png, jpg, or PDF format not more than 10MB.

Step 8: Verify OTP, review the summary, and click Submit.

A tracking number will be sent via email and SMS.

VUL fund withdrawals take five (5) business days upon submission of your complete requirements.

Yes, you will be notified of each status change to your VUL fund withdrawal request through the mobile app, as well as through email and SMS notifications. If you fail to receive an update, please call our Client Care hotline at (02) 8849-9888 for assistance.

Clients may opt for a full withdrawal. However, we highly discourage withdrawing from your VUL fund as this surrenders your policy, especially during periods of poor performance. Most VUL funds are market-driven and require time to show potential earnings.

If the intention is for a policy surrender, this will be processed differently via the Policy Surrender process in any Client Service Center.

Not yet. However, we are currently working on making this available on the website soon.

No, you can only withdraw from one (1) VUL policy at a time per transaction.

For security reasons, you cannot file another fund withdrawal from the same VUL policy if it has an ongoing withdrawal request in the mobile app.

You may request another OTP via Email. If the issue persists with both options, you may contact our Client Care hotline at (02) 8849-9888 for assistance.

To cancel an ongoing VUL fund withdrawal request, please reach out to our Client Care hotline at (02) 8849-9888 for assistance.

Yes, an SMS notification will be sent to your registered mobile number once your fund withdrawal request has been approved or denied.

Yes, you will receive an email and SMS notification through your registered contact details to inform you of the next steps that you need to do via the Service Request Tracker (SRT) in the Sun Life PH mobile app.

VUL fund withdrawals via the Sun Life PH mobile app can only be processed in the Philippines.

If you need to make a fund withdrawal while you are out of the country, please contact our Client Care hotline or your financial advisor.