Is your portfolio weather proof?

How inflation and interest rates affect your portfolio

Imagine heading out for the day without checking the weather first. It starts out warm and sunny. But later in the day, the skies darken and heavy rain begins. Without an umbrella or jacket, you’re suddenly caught off guard. Today’s market environment is very much like that. Markets could shift quickly and unexpectedly. And while many portfolios are designed for “sunny days” not all are prepared when conditions suddenly change.

Shifting market environment

Investing today has also become more complex and uncertain. Markets are influenced by forces that are more dynamic, and sometimes unpredictable. A perfect example of this was the recent geopolitical tensions between the US-Iran. The war disrupted oil flows which caused energy prices to skyrocket. Spiking energy prices drove inflation and interest rates higher.

These aren’t just economic terms that are relevant to investors and portfolio managers. They directly impact everyday life. I am sure you’ve seen how much your electric bill has become more expensive (coupled with Manila’s heat, ours has increased to more than 1.5x) or how much your weekly groceries have jumped. Understanding these can help you better manage your budget and understand what’s happening to your portfolio.

![]()

Inflation: The heat that gradually builds

Inflation refers to the gradual increase in prices over time.

You’ve likely felt this already. The cost of food, fuel, travel, and other daily expenses steadily increases year by year. Periods like the 2022 Russia-Ukraine war and 2025 US-Iran war made these changes even more palpable, putting pressure on corporates, households and investors.

It is like the heat on an unusually warm day. At first, the weather feels manageable. But as the day goes on, the temperature slowly rises. Without realizing it, the heat starts to feel uncomfortable—and eventually draining.

In the same way, inflation builds gradually. It may not feel significant at the beginning, but over time, it reduces what your money can buy.

Even if your savings remain unchanged, your purchasing power weakens as prices continue to rise. This creates an important reality for investors. Just staying in the shade (keeping your money in cash) may not be enough. You need ways to grow your wealth so it can keep up with the rising “heat” of inflation.

![]()

Interest Rates: Controlling the Temperature in the Economy

If inflation is like rising heat in the environment, then interest rates are how policymakers try to control that temperature.

A simple way to think about it is this. Interest rates act like the cooling system of the economy. When the economy starts to “overheat”— with inflation rising too quickly —central banks raise interest rates to help cool things down. When economic activity slows too much, they lower interest rates to stimulate growth. This is exactly what is happening now. As inflation runs “hot”, central banks have been decisive in raising interest rates.

How do these policy shifts translate into our everyday lives?

When interest rates go up, the economy cools down.

Borrowing becomes more expensive

Businesses may delay expansion

Consumers spend more cautiously

Conversely, when interest rates go down, the economy warms back up.

Loans become cheaper

Businesses invest more

Consumer spending and economic activity increase

These changes aren’t only felt in the real economy. They produce a ripple effect on financial markets as well. Rising rates can put pressure on stock prices as borrowing costs increase and valuations compress. Also, hurdle rates for investment become higher. Therefore, only a handful get pursued by corporates.

In a nutshell, interest rates help regulate how fast or slow the economic environment is moving—and that, in turn, influences how your investments perform.

The challenge is that inflation and interest rates do not move in a straight line. They can rise faster than expected, stay elevated longer than anticipated, or shift direction without warning. Markets also tend to anticipate these changes—often reacting ahead of the actual data. It is like planning your day based on a sunny forecast but later on encountering rain. This unpredictability makes it harder to rely on a single strategy or assume that conditions will stay static.

![]()

Building a Portfolio for All Seasons

In an uncertain world, the goal is not to perfectly predict what will happen next. That’s extremely difficult—even for experienced investors. Instead, the goal is to prepare for different scenarios. A more resilient portfolio includes --- a mix of different types of assets (fixed income, equities, alternatives), diversified across different markets and sectors, balanced opportunities for growth, income and stability.

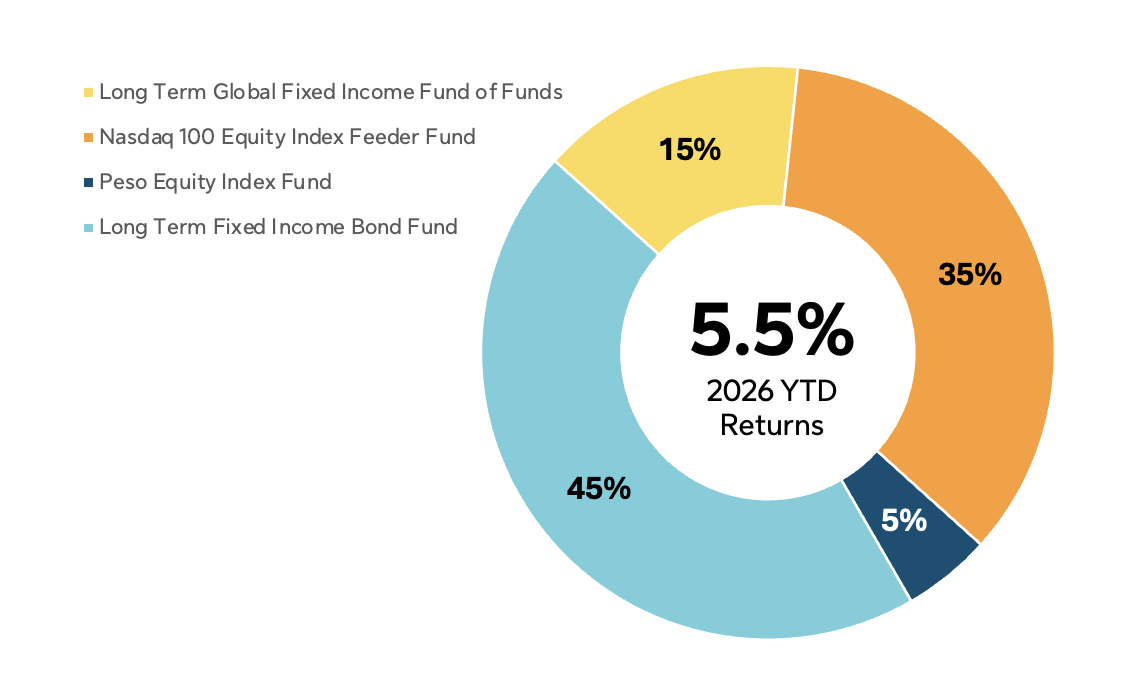

Current bRight Mix Portfolio: 2026 Year to Date Return: 5.5%

* Returns are as of May 15, 2026

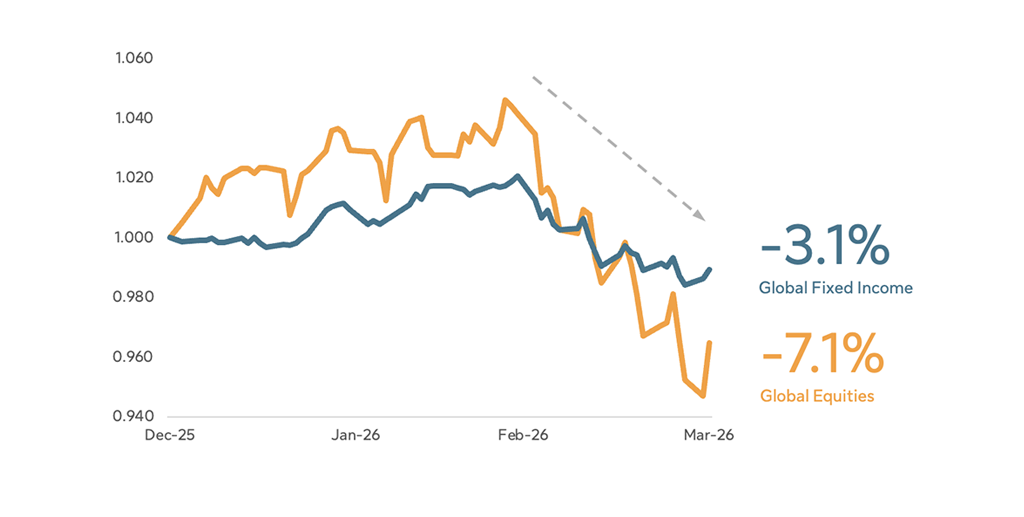

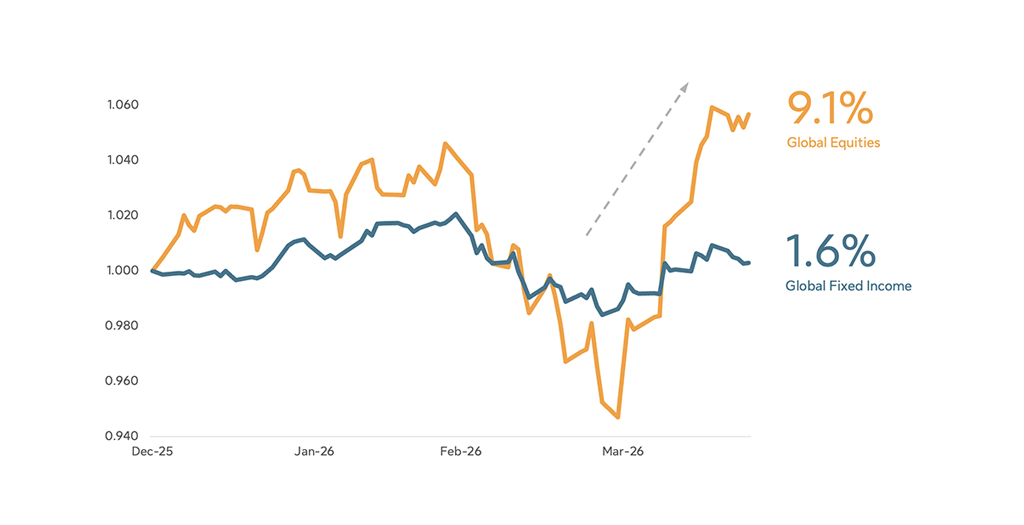

Another important principle in withstanding volatility is staying invested. Investors often try to time the market. But this is very difficult to execute. As we’ve seen both drops and subsequent recoveries could be sudden. In fact, the recovery post US-Iran war took only 15 days before it reached its pre-war highs. Missing just a few of the strongest days in this reversal can significantly impact overall returns. We believe that consistency and discipline matter more than trying to time the market perfectly.

Market drop after start of US-Iran war

Market recovery 15 days after the low

Staying Prepared: The Next Step

Now may be a good time to reflect. “Is my portfolio built only for ideal conditions—or is it ready for whatever comes next?” Regardless of your answer, it might be useful to review your current allocation. Ensure you are properly diversified. And take steps to prepare—not just for the good times, but for all market conditions. If you are lost or are unsure what to do, it might be useful to contact your Sun Life advisor. They would be more than willing to guide you through this process. Because investing, as in life, it’s not about predicting the weather. It’s about being ready for it.