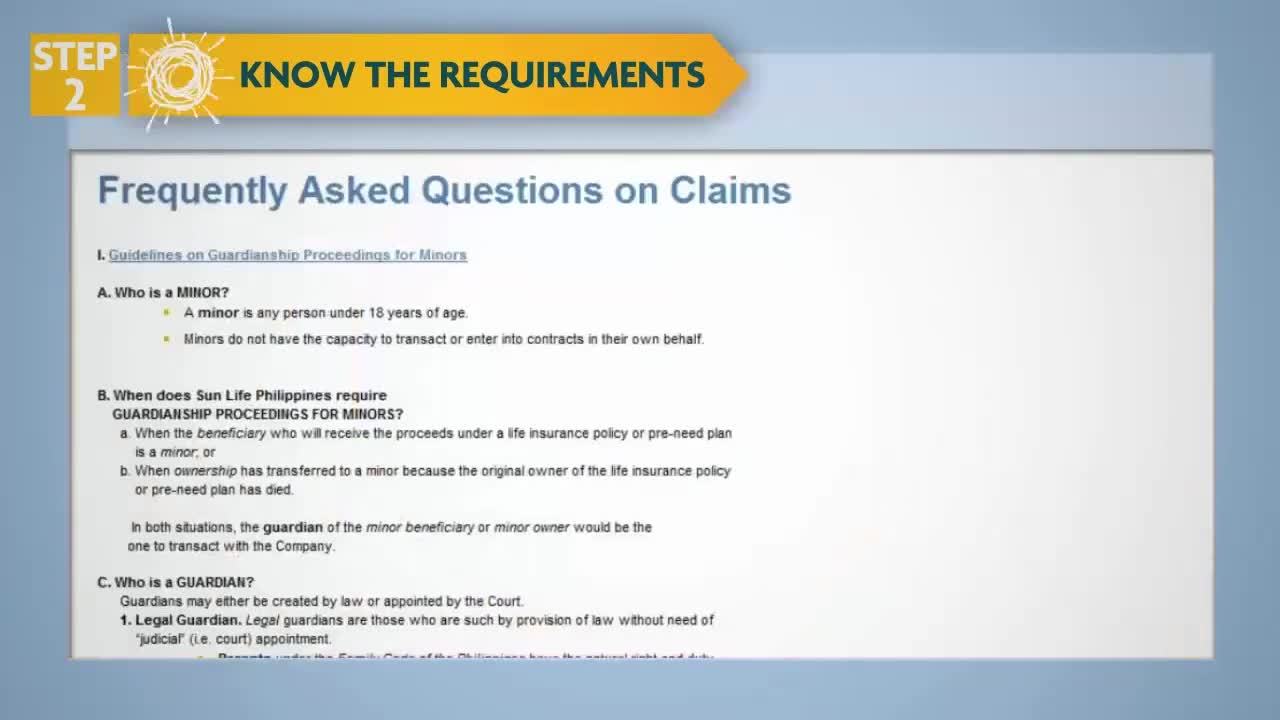

I. Guidelines on Guardianship Proceedings for Minors

II. What will happen if the primary beneficiary dies?

A. If there is one (1) primary beneficiary

1. If the primary beneficiary pre-deceases (dies ahead of) the insured, the death claim proceeds shall be paid to the Contingent beneficiary/ies

a. What if there is no contingent beneficiary?

The death claim proceeds shall vest on the estate of the insured. (See “Guidelines on Settlement of Estates”)

2. If the life insured pre-deceases the primary beneficiary and then subsequently the primary beneficiary dies before the claim is settled, the death claim proceeds shall vest on the estate of the primary beneficiary.

B. If there are two (2) or more primary beneficiaries

1. If one (1) primary beneficiary pre-deceases the insured, proceeds shall be paid to the surviving primary beneficiary/ies.

2. If all the primary beneficiaries pre-decease the insured, proceeds shall be paid to the contingent beneficiary/ies.

a. What if there is no contingent beneficiary?

The death claim proceeds shall vest on the estate of the insured upon the insured’s death.

3. If the life insured pre-deceases the primary beneficiaries and subsequently one or some of the primary beneficiaries die before the death claim is settled, the proceeds shall be paid to the surviving primary beneficiary/ies and to the estate of the deceased primary beneficiary/ies.

4. If the life insured pre-deceases all the primary beneficiaries and subsequently all of the primary beneficiaries die before the death claim is settled, proceeds shall vest on the estates of all the primary beneficiaries

C. What are the rights of the contingent beneficiaries?

Contingent beneficiaries, if living, are entitled to receive the death claim proceeds only when all the primary beneficiaries had died ahead of the life insured

III. Naming the spouse as beneficiary

A. What to submit on top of the basic requirements?

- If married, submit Marriage Contract issued by the National Statistics Office (NSO) or Philippine Statistics Authority (PSA)

- If not married and both parties do not have legal impediment to marry, submit

- Affidavit re No legal impediment** to marry [form may be secured from Claims Services]

- Certificate of No Marriage (CENOMAR) of both parties issued by the National Statistics Office (NSO) or Philippine Statistics Authority (PSA)

- ** Both parties are free to marry i.e. they have never been previously married

IV. What will happen if there is a legal impediment to marry?

Civil Code

“Art 739. Donation is void if it is made between people guilty of adultery/concubinage at time of donation, between people guilty of criminal offense and to a public officer and his family by reason of his office.”

“Art 2012. Any person who is forbidden from receiving any donation under article 739 cannot be named beneficiary of a life insurance policy by the person who cannot make any donation to him, according to said article.”

If the common law spouse is the sole primary death beneficiary

- If there is a contingent beneficiary, the proceeds shall be paid to the contingent beneficiary.

- If there is no contingent beneficiary, the proceeds shall vest on the estate of the insured.

If there are two or more primary death beneficiaries.

The proceeds shall be distributed to other primary beneficiaries.

V. When a spouse is named as a primary beneficiary, what will happen in case the marriage was annulled after the policy had been issued and the Policyowner-insured failed to change the beneficiary designation prior to his/her death?

The share of the designated spouse-beneficiary shall still be payable to him/her once the claim requirements have been completed because at the time he/she was designated as a beneficiary of the policy, the marriage was still valid.

- Naming “Children Borne of this Marriage” as beneficiaries

A. What to submit on top of the basic requirements?

1.Affidavit re name, number and birth dates of the children borne of the marriage between the spouses

2.Certified true copy of the children’s Birth Certificate

B. What if there is a minor child?

Refer to Guidelines on Guardianship Proceedings for Minors

- What to do when claim proceeds become payable to the estate?

- To whom will the ownership of the policy be transferred after the death of the initial owner?

A. To whom will the ownership be transferred?

1. For juvenile policies (policies issued on the life of a minor)

Ownership will automatically be transferred to the life insured once the initial owner dies, regardless if there is an irrevocable beneficiary.

Note: The “juvenile” policy still requires that the minor owner deal through his/her guardian for any policy transaction (e.g. applying for an advance, changing the beneficiaries, etc.)

2. For adult policies (policies issued on the life of an adult purchased by another adult)

Ownership will automatically be transferred to the life insured once the initial owner dies, regardless if there is an irrevocable beneficiary.

B. How to request for transfer of ownership?

1. If there is an in-force Premium Coverage Upon Death or Disability of Initial Owner (WPDD, WPD or CSEPC for Sun Heritage Plans) attached to the policy, there is no need to request for the transfer of ownership. Since a claim for these benefits will be filed, the transfer of the ownership of the policy will be communicated by the Claims Services to the Policy and Plan Change Section once the certified true copy of the initial owner’s Death Certificate is received.

(See list of requirements above or click on this link to download the Requirements Checklist for Waiver of Premium)

2. If there is no in-force Premium Coverage Upon Death or Disability of Initial Owner (WPDD, WPD or CSEPC for Sun Heritage Plans) attached to the policy, a certified true copy of the Death Certificate has to be forwarded to the Policy and Plan Change Section so transfer of ownership may be processed.

- Guidelines on Guardianship Proceedings for Incompetents

- IMPORTANT NOTE:

Sun Life has issued the Guidelines on Guardianship Proceedings for Minors, Incompetents and Settlement of Estates merely as a general tool for the assistance of claimants. These guidelines do not and are not meant to serve as legal advice to claimants. Claimants are advised and encouraged to seek legal advice of their own.